1% Captures Half of Capital Gains Tax Benefits

New budget data reveals how capital gains tax and negative gearing disproportionately benefit the wealthiest 1% of earners, fueling housing speculation.

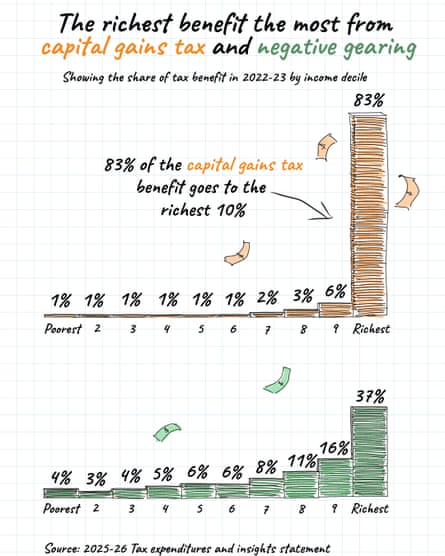

The latest federal budget analysis reveals a striking disparity in how capital gains tax concessions are distributed across Australian income earners, with data showing that more than half of the benefit from the CGT concession flows directly to the top 1% of income earners. This concentration of tax benefits raises important questions about equity and fairness in the tax system, particularly as policymakers grapple with housing affordability and wealth inequality.

The current year's federal budget introduces significant changes to negative gearing policies, capital gains tax arrangements, and discretionary trust tax concessions—measures that critics argue have inadvertently fueled property speculation while predominantly benefiting Australia's wealthiest households. These tax provisions have become increasingly controversial as they interact with broader housing market dynamics and contribute to wealth concentration among high-income earners. Understanding the impact of these policies requires examining both their stated intentions and their actual distributional effects across different income groups.

According to the most recent budget documents, the top 1% of lifetime earners have accumulated more than $700,000 in cumulative tax concessions over their working lives specifically through capital gains tax advantages, negative gearing deductions, and discretionary trust tax benefits. This staggering figure underscores the magnitude of wealth being protected through these tax mechanisms and highlights how structural features of the tax code can amplify existing wealth disparities. The concentration of these benefits among the highest earners suggests that the tax system may inadvertently be reinforcing rather than mitigating wealth inequality.

The negative gearing provisions allow property investors to deduct losses from rental properties against their other income, effectively creating tax shields that are most valuable to those in higher tax brackets. This mechanism was originally designed to encourage investment in rental properties and support housing supply, but evidence suggests it has instead contributed to speculative property investment and inflated asset prices. High-income earners benefit disproportionately from negative gearing because they have larger tax liabilities to offset and more capital to invest in multiple properties.

Capital gains tax concessions further advantage wealthy investors through the 50% discount on capital gains applied after holding an asset for more than one year. This discount substantially reduces the effective tax rate on investment returns compared to ordinary income, creating powerful incentives for wealth accumulation through asset appreciation rather than wage earnings. When combined with negative gearing deductions, these provisions create a potent combination that substantially reduces the tax burden on property investors while ordinary workers pay full marginal tax rates on their earnings.

Discretionary trust structures represent another layer of tax planning available primarily to wealthy families seeking to minimize their collective tax obligations. These trusts allow high-income earners to distribute investment income across family members in lower tax brackets, effectively fragmenting income to take advantage of progressive tax rates. The interaction between trust income distribution rules and capital gains tax discounts creates sophisticated planning opportunities that require specialized tax advice to execute, inherently favoring those with resources to engage professional advisors.

Critics argue that these interconnected tax concessions have fundamentally distorted the property market, transforming housing from primarily a consumption good into a speculative investment vehicle. The tax advantages create powerful economic incentives for investors to acquire multiple properties, driving up prices and reducing housing availability for owner-occupiers and first-time buyers. This shift in market dynamics has contributed to declining housing affordability across Australia's major cities and exacerbated generational wealth gaps between property-owning and non-owning cohorts.

The distributional analysis presented in recent budget documents provides empirical evidence that these tax concessions function as a regressive transfer from the broader taxpaying population to the most affluent households. While policymakers have historically justified these provisions as necessary to encourage investment and housing supply, the evidence increasingly suggests they primarily benefit existing investors and inflate property values without meaningfully expanding housing stock. The $700,000 figure for top 1% earners represents foregone government revenue that could alternatively be allocated to affordable housing programs, healthcare, education, or infrastructure investments benefiting broader society.

Recent policy discussions have centered on potential reforms to these tax provisions, with proposals ranging from reducing the capital gains tax discount to limiting negative gearing deductions for new investments. Some proposals suggest grandfathering existing arrangements while preventing future investors from accessing the same benefits, while others advocate for more comprehensive reform eliminating these concessions entirely. The political challenge lies in balancing concerns about fairness and budget sustainability against property industry lobbying and the resistance of current beneficiaries to reduced tax benefits.

International comparisons reveal that Australia's approach to capital gains taxation is relatively generous compared to many other developed economies, many of which either tax capital gains at full marginal tax rates or apply higher effective tax rates through different mechanisms. This international context suggests that Australia's current approach may reflect political choices favoring asset owners over wage earners, rather than economic necessity. Policymakers in other jurisdictions have implemented more comprehensive capital gains taxation without apparent harm to investment or economic growth, suggesting that reform options exist that could broaden the tax base while maintaining investment incentives.

The housing market impacts of these tax provisions deserve particular scrutiny given Australia's acute housing affordability crisis. Properties that serve as investment vehicles rather than homes for primary residence generate tax-advantaged returns that ultimately reflect higher property valuations reducing housing accessibility for non-investors. The feedback loop between tax benefits encouraging investment, investment increasing demand, and increased demand driving higher prices has demonstrably disadvantaged younger Australians and lower-income households systematically excluded from property investment opportunities.

Future budget deliberations will likely continue examining these tax concessions and their distributional impacts. The evidence presented in budget documents provides policymakers with clear data showing that current arrangements heavily concentrate benefits among the wealthiest Australians, raising questions about the equity and efficiency of maintaining these provisions indefinitely. Whether political will exists to implement meaningful reform remains uncertain, but the empirical case for reconsidering these arrangements has strengthened considerably as wealth inequality concerns gain prominence in public discourse.

Understanding the full scope of these tax benefits' impacts requires examining not just their immediate fiscal costs, but also their broader effects on wealth distribution, housing markets, and economic opportunities across society. The concentration of capital gains tax benefits among top earners highlights how tax policy choices can either mitigate or amplify market-driven inequality. As policymakers continue evaluating Australia's tax system, the evidence increasingly suggests that reform deserves serious consideration to address both fiscal sustainability and distributional fairness concerns.