Inflation Surges: Impact on Flights, Food & Fuel

Latest inflation figures show significant increases in flights, food, and fuel costs. Discover what rising inflation means for borrowers and savers across the nation.

The latest inflation figures reveal a concerning upward trajectory across multiple sectors of the economy, with particular pressure mounting in three critical areas: air travel, grocery prices, and energy costs. As consumers navigate an increasingly expensive marketplace, understanding these inflation trends becomes essential for household budgeting and financial planning. The data paints a complex picture of economic pressures that extend far beyond simple price increases at the pump or supermarket checkout.

Air travel has emerged as one of the most visible casualties of rising inflation, with ticket prices climbing substantially as airlines grapple with elevated fuel costs and labor expenses. The aviation industry, which struggled through pandemic-related disruptions, now faces renewed pressure from inflationary forces that show no signs of abating in the near term. Consumers planning vacations or business trips are increasingly shocked by the premium prices required to secure seats, fundamentally altering travel behavior and vacation budgets for many families across the country.

Fuel prices represent a critical driver of broader inflation pressures, affecting not just transportation costs but rippling through the entire supply chain. Gasoline and diesel prices influence everything from shipping costs to heating expenses, creating a cascading effect throughout the economy. Energy sector volatility continues to present challenges for policymakers seeking to understand and manage inflationary forces in a rapidly changing global landscape.

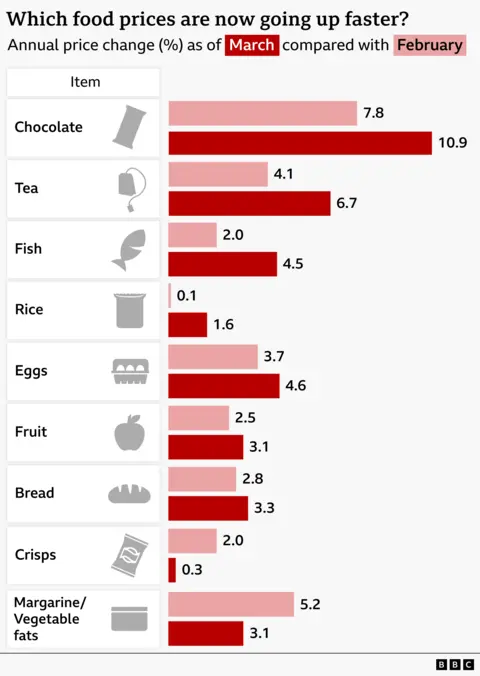

Food prices have reached levels that demand serious attention from household budget managers everywhere. Grocery bills have climbed considerably over recent months, placing significant strain on families already managing tight financial constraints. Staple items across all categories—from produce to proteins to dairy—have seen substantial price increases that accumulate meaningfully when multiplied across weekly shopping trips.

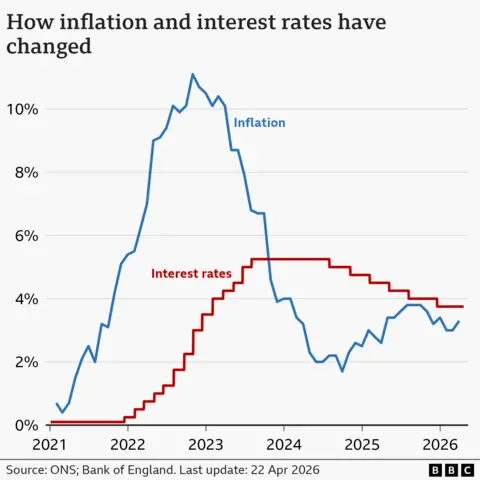

Understanding the mechanics of inflation's impact on consumers requires examining how these price increases translate into real-world consequences for household finances. For borrowers carrying variable-rate debt, inflation often signals upcoming interest rate increases from the Federal Reserve, which can substantially raise monthly payment obligations. This creates a precarious situation where both the cost of goods and the cost of borrowing simultaneously climb, squeezing household budgets from multiple directions.

The relationship between inflation and interest rates presents a nuanced challenge for economic decision-makers. Central banks typically respond to persistent inflation by raising benchmark interest rates, which banks then pass along to consumers through higher rates on adjustable mortgages, credit cards, and other variable-rate products. These interconnected forces create a challenging environment where consumers must carefully evaluate their borrowing decisions and consider locking in fixed rates before they rise further.

For savers, inflation presents a paradoxical situation where the purchasing power of accumulated wealth gradually diminishes unless savings earn interest rates that exceed the inflation rate. Traditional savings accounts offering minimal interest rates essentially guarantee that money saved today will be worth less in real terms tomorrow. This dynamic incentivizes savers to seek alternative investment vehicles or higher-yield savings products to protect their financial security.

Regional variations in inflation rates add another layer of complexity to the national picture. Some areas experience significantly more pronounced price increases in certain categories than others, reflecting differences in local supply chains, transportation costs, and regional economic conditions. Understanding your specific local inflation environment becomes crucial for accurate financial planning and budgeting at the household level.

The trajectory of future inflation expectations remains a subject of intense debate among economists and policymakers. Some analysts predict that inflation will gradually moderate as supply chain disruptions resolve and monetary policy tightens, while others warn that structural economic changes could lead to persistently elevated price levels. These divergent predictions create significant uncertainty for consumers and businesses attempting to plan ahead with limited information about the economic future.

Wage growth presents another critical dimension of the inflation equation. When workers' wages fail to keep pace with rising prices, real purchasing power declines and living standards effectively deteriorate despite nominal income remaining stable. The question of whether wage increases will eventually catch up with inflation, or whether workers will experience persistent erosion of their buying power, remains hotly contested in economic circles and has profound implications for millions of households.

Specific sectors show varying degrees of inflation pressure, with some industries experiencing dramatic price escalation while others remain more stable. Understanding these sectoral differences helps consumers identify which budget categories require the most aggressive cost management and where flexibility exists. Energy and food remain persistently expensive, while some technology and service sectors show more moderate price growth.

Financial planning strategies must adapt to inflationary environments through diversified approaches addressing both immediate budget constraints and long-term wealth preservation. Consumers should evaluate their borrowing strategies to ensure they secure favorable rates before they rise further, while simultaneously seeking savings vehicles that provide returns exceeding inflation. This balanced approach helps protect financial security across multiple timeframes and economic scenarios.

Fixed-income investors face particular challenges during inflationary periods, as the real returns on bonds and similar securities decline when inflation exceeds interest rates. Traditional investment wisdom suggests reconsidering portfolio allocation to include inflation-protected securities or assets likely to appreciate alongside rising prices. These adjustments help preserve long-term wealth accumulation despite temporary economic headwinds.

The broader implications of sustained inflation extend beyond individual household finances to encompass macroeconomic stability and social equity. Inflation disproportionately affects lower-income households that spend larger percentages of their income on necessities like food and fuel, widening existing economic inequality. Understanding this distributional impact becomes important for policymakers designing responses to inflationary pressures.

Looking forward, the key question remains how high inflation will climb before moderating or accelerating further. This uncertainty complicates planning for consumers, businesses, and policymakers alike, all operating with incomplete information about future economic conditions. Staying informed about inflation data releases and adjusting financial strategies accordingly remains essential for navigating this challenging economic environment with confidence.

The latest inflation figures underscore the importance of proactive financial management in an uncertain economic climate. Whether you're a borrower evaluating loan options, a saver seeking appropriate investment vehicles, or a consumer managing daily expenses, understanding inflation's impact on your specific financial situation empowers better decision-making. By staying informed and adaptable, households can work toward maintaining their financial security despite persistent inflationary pressures affecting the broader economy.

Source: BBC News